In today’s rapidly evolving world, technology has permeated every aspect of our lives, and the lending industry is no exception. When it comes to auto loans, technology has brought about a transformative shift, revolutionizing various aspects of the lending process and ushering in a new era for the industry.

Auto lending plays a pivotal role in helping individuals and businesses acquire vehicles through loans provided by financial institutions. However, the traditional auto lending process was burdened with lengthy paperwork, manual underwriting, and limited options for borrowers. This is where technology stepped in, reshaping the landscape and making it more efficient, convenient, and accessible.

Technology has revolutionized the autofinance industry, fundamentally transforming various aspects of the lending process. By streamlining loan applications, enhancing the customer experience, mitigating risks and fraud, and improving efficiency and cost savings, technology has left an indelible mark on auto lending.

Streamlining Loan Applications

The popularity of online loan applications has soared, offering borrowers a convenient and time-saving alternative. In 2022, a noteworthy study conducted by Experian revealed that online applications comprised a significant 51% of all auto loan originations. This statistic underscores the escalating preference for digital channels among borrowers. However, the advantages of online loan applications extend beyond borrowers; lenders also reap efisubstantial bents. By embracing online applications, lenders enhance their ability to efficiently receive and process loan requests. The streamlined data collection process minimizes manual errors and bolsters overall operational efficiency. Consequently, this newfound efficiency translates into expedited loan processing times, a favorable outcome for both lenders and borrowers alike.

Automated Underwriting Systems

Automated underwriting systems have expedited the loan approval process, saving time and improving customer satisfaction. These systems analyze borrower data, credit scores, and financial history, enabling lenders to make quicker lending decisions. Borrowers experience reduced waiting times, and the overall loan approval process becomes more efficient. Automated underwriting systems utilize advanced algorithms and machine learning to assess creditworthiness more accurately. This data-driven approach results in fairer lending decisions, reducing the risk of human bias and ensuring a level playing field for borrowers.

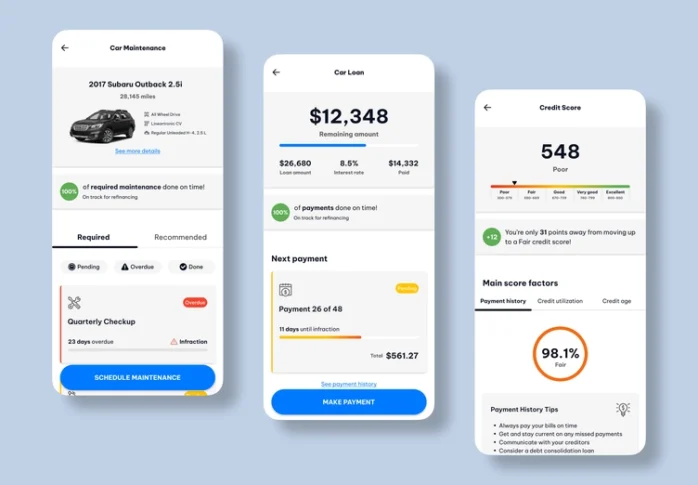

Enhancing Customer Experience

Advancements in technology have given borrowers the ability to access vast amounts of information about different vehicles and financing choices, empowering them in the process. Online research and comparison tools have proven to be invaluable assets for borrowers. According to a survey conducted by JD Power, a staggering 83% of auto loan borrowers utilized the internet to explore and compare their loan options. The introduction of digital loan management platforms has revolutionized how borrowers handle their accounts, providing them with a centralized and user-friendly interface. These platforms allow borrowers to effortlessly view their payment schedules, make payments, and track the progress of their loans. Moreover, technology enables seamless communication channels between borrowers and lenders, resulting in improved customer service and responsiveness.

Risk Mitigation and Fraud Prevention

The utilization of advanced data analytics in technology has revolutionized the assessment of borrower risk profiles, enabling lenders to make more precise lending decisions while minimizing the risk of default. By harnessing the power of big data, lenders can evaluate risk profiles with greater accuracy, resulting in well-informed lending choices. Advanced data analytics have proven invaluable in identifying patterns and anomalies that may indicate fraudulent activities. Through the monitoring of borrower behavior and transactional data, technology aids lenders in detecting and preventing fraud, thereby safeguarding the interests of both borrowers and lenders. The integration of identity verification technologies, such as biometric authentication methods, has significantly enhanced security in the auto lending process. According to a study conducted by Javelin Strategy & Research, the incorporation of biometrics reduces fraud by up to 80%, instilling confidence and peace of mind in both borrowers and lenders.

Improving Efficiency and Cost Savings

Technology has automated the loan document generation process, reducing paperwork and minimizing the likelihood of manual errors. This streamlining of the loan origination process improves efficiency for both borrowers and lenders, saving time and resources. The automation of loan document generation has had a profound impact on efficiency and cost savings. A study conducted by Accenture found that digitizing loan documents can reduce processing costs by up to 70%. This automation not only saves time but also minimizes the likelihood of manual errors, improving accuracy and customer satisfaction. Digital payment systems have provided borrowers with convenient payment options, including online portals and mobile apps. This flexibility improves the overall borrower experience and ensures timely payments. For lenders, digital payment systems streamline loan servicing operations, reducing administrative burden, improving accuracy, and ensuring efficient cash flow management.

Challenges and Future Trends

As technology advances, data security and privacy concerns become increasingly important. Lenders must prioritize robust cybersecurity measures to protect borrower information and prevent data breaches, safeguarding the trust of their customers. The auto financing industry is subject to evolving regulatory requirements. Lenders need to stay updated and ensure compliance with relevant regulations to avoid legal and reputational risks. Adapting to the changing regulatory landscape is crucial for lenders to maintain a competitive edge. Looking ahead, the future of auto lending technology holds promising possibilities. Artificial intelligence, auto loan management software, and decentralized finance (DeFi) are expected to further transform the industry, enhancing automation, transparency, and efficiency. According to a report by Allied Market Research, the global AI in the automotive industry is projected to reach $12.55 billion by 2027, underscoring the significance of these advancements.

Conclusion

Technology has revolutionized the auto lending industry, bringing unprecedented improvements to the lending process. Through streamlining loan applications, enhancing the customer experience, mitigating risks and fraud, and improving efficiency and cost savings, technology has reshaped the industry. The integration of technology has resulted in faster loan approvals, improved customer experiences, enhanced risk management, and greater operational efficiency. As technology continues to advance, its role in the autofinance industry will become increasingly integral. To stay competitive and provide exceptional service to borrowers, lenders must embrace innovative solutions, prioritize data security, and adapt to regulatory changes. By doing so, they can seize the opportunities presented by technology and shape the future of auto lending for the benefit of all stakeholders.

")